Annual Market Review: 2025

A Year of Strength Amid Uncertainty

If 2025 had a defining theme, it was resilience against the odds. Investors navigated sweeping tariffs, sticky inflation, geopolitical conflicts, a prolonged government shutdown, and a cooling labor market—yet markets finished the year firmly higher. Strong consumer spending, record corporate profitability, and the continued artificial intelligence boom helped offset economic and political headwinds.

Markets Look Past Volatility

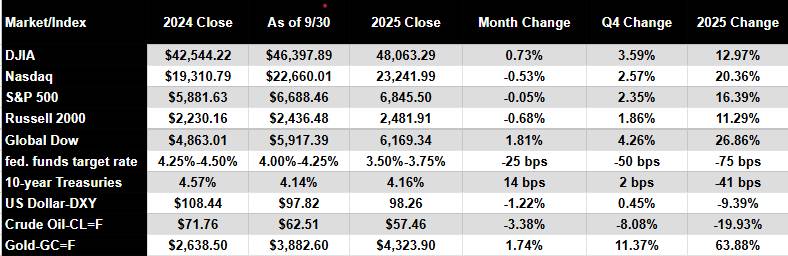

The year began calmly but took a sharp turn in April following new tariff announcements that rattled investors and sparked a brief selloff. Volatility spiked, the U.S. dollar weakened, and even Treasury bonds struggled as yields moved higher. As trade tensions eased later in the year and corporate earnings remained strong, confidence returned. By year-end, all major U.S. stock indexes posted solid gains, with technology and AI-driven companies leading the way. Global markets also had a standout year. After several years of U.S. dominance, international blue-chip stocks surged, with Europe and parts of Asia delivering impressive returns. The Global Dow significantly outperformed U.S. indexes, reflecting broad-based global strength.

The Fed Shifts Course

Inflation remained stubborn throughout much of 2025, hovering near 3%—above the Federal Reserve’s 2% target. Rising import costs from tariffs and elevated food and energy prices kept pressure on consumers. As the labor market softened and job growth slowed, the Fed pivoted in the second half of the year, cutting interest rates three times beginning in September. By year-end, the federal funds rate had been reduced by 0.75%, bringing borrowing costs to their lowest level since 2022. Looking ahead, the Fed has signaled a cautious stance, projecting only one additional rate cut in 2026 as it balances inflation risks with slowing economic momentum.

Economy Grows, but Unevenly

Despite early volatility, the U.S. economy expanded in 2025, with GDP growth estimated around 1.8%–2.0%. Growth accelerated sharply i n the third quarter before moderating late in the year. Consumer spending remained the backbone of economic activity, increasingly driven by higher-income households. Business investment—particularly in AI and software—helped counter weakness in manufacturing and housing. The labor market showed clear signs of cooling. Unemployment rose to approximately 4.6% by November, hiring slowed, and wage growth moderated to about 3.5%. While layoffs remained historically low, fewer job openings made it more challenging for job seekers.

Corporate Earnings Drive Optimism

Corporate America delivered impressive results in 2025. S&P 500 earnings grew by more than 12%, well above the long-term average, while profit margins reached their highest level since 2008. Revenue growth also exceeded historical norms, reinforcing investor confidence and helping propel markets higher despite economic uncertainty.

Stock Market Indexes

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Bonds, Oil, and Gold Tell a Different Story

While stocks moved higher, other asset classes reflected a more cautious backdrop. Bonds delivered modest but positive returns as interest rates declined later in the year, providing stability and income for investors. Oil prices fell nearly 20% amid record U.S. production and cooling global demand. In contrast, gold surged to record highs, posting one of its strongest years in decades as investors sought protection from inflation, dollar weakness, and geopolitical uncertainty. The U.S. dollar experienced its steepest annual decline in years, pressured by fiscal concerns, tariffs, and shifting rate expectations.

In Summary

2025 proved that markets can adapt—even thrive—amid uncertainty. Strong earnings, a resilient consumer, and a supportive shift in monetary policy helped drive gains across equities, while bonds resumed their role as a stabilizer. Inflation and labor market trends remain key areas to watch as we head into 2026, but the year closed with more progress than setbacks.

We will continue to monitor economic and market developments and how they may impact your financial plan. Please reach out if you’d like to discuss what these trends mean for you.

Office Update

As we head into the new year, we’d like to take a moment to express our appreciation to everyone who joined us for our open house. It was great connecting with you, celebrating a successful move, and sharing our new space together. For those who haven’t yet had the opportunity to visit our new office, we look forward to welcoming you in 2026.

Your Financial Focus Team

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources ( i.e., wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not come to pass. U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 largest, publicly traded companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indexes listed are unmanaged and are not available for direct investment.